Love is in the air!

Here is our favorite love story ... about two of our best friends in the nonprofit world. Their names are Fundraising and Finance. __________________________________________________________________________________________________________ Our friend Finance is not so sexy :) But he is intelligent, organized and precise. Fundraising is way hotter than Finance. She’s exciting, inspiring, and passion-driven. And everyone loves to focus their attention on her. When you invite Fundraising to dinner, Finance has to come along. (The good news is, Finance always picks up the tab. Ha!) Fundraising will make your heart melt with the stories she tells and her big energy and hope. But at dinner Finance will talk about cash flow, budgeting, operating reserves, and payroll expenses. You know, all the pesky little details that actually matter. Who invited that person? Sheesh! We know. Finance isn’t sexy, but Fundraising without Finance is just short-sighted. At first, they seem like an unlikely couple but Fundraising and Finance are intimates. Their nonprofit home is a happy, efficient, sustainable, and well-funded place to be. Like all couples, they can struggle. But when they work together with open continuous communication and feedback, they are an unstoppable team. That, our friends, is a nonprofit love story. ___________________________________________________________________________________________________________ Q: So, what’s the moral of the story? A: To build nonprofit sustainability, your finance and fundraising teams must collaborate closely and communicate on a continuous basis. [Read: What Fuels Nonprofit Sustainability] Financial stewardship builds sustainable organizations. But many nonprofit leaders are more versed in fundraising, marketing and events. That’s why Blue Fox exists – to organize, empower and educate nonprofit leaders on all thing’s financial management. We’ve got your back!

0 Comments

Here’s a tax legislation win-win!

If you have student loans, your employer now has the opportunity to provide repayment assistance through 2025 tax-free. Let’s say that again: tax-free! An article published by SHRM explains: “The Consolidated Appropriations Act, 2021 (CAA), signed into law by President Donald Trump on Dec. 27 extends for five years COVID-19 relief that allows employer-provided student loan repayment as a tax-free benefit to employees under Section 127 of the Internal Revenue Code. Through 2025, employers can continue to make contributions of up to $5,250 per employee annually toward eligible education expenses, like tuition or student loan assistance, without raising the employee's gross taxable income.” SHRM calculates that only 8% of employers provide loan assistance. This legislation aims to improve that number to make a dent in our nation’s student loan debt crisis. Chatrane Birbal, vice president for public policy at SHRM said, "This benefit will provide some relief to employees who are currently repaying student loan debt and also gives employers more flexibility in the design of benefit offerings for recruitment and retention purposes." Let’s spread the word and keep our fingers crossed that more employers recognize the win-win benefits of offering tuition repayment assistance now, through 2025 and beyond.  Your tax refund may come later this year.

#whatthefox is right! If you frequent the IRS.gov virtual newsroom (like we do), you’ll discover these facts: “The Internal Revenue Service announced that the nation's tax season will start on Friday, February 12, 2021, when the tax agency will begin accepting and processing 2020 tax year returns. The February 12 start date for individual tax return filers allows the IRS time to do additional programming and testing of IRS systems following the December 27 tax law changes that provided a second round of Economic Impact Payments and other benefits.” Although shocking and unprecedented, the IRS has reason (outlined in this full article): to make sure people eligible for stimulus money, receive those funds before filing their taxes. That’s nice - we’ll let them slide this year. We encourage you to read the IRS’s latest news release for simple steps to speed your refund and a full list of key filing season dates. As we’ve said before, our team at Blue Fox is up to speed on the latest tax law changes, and there are a lot. As you can imagine, tax preparation has never been more complex or intricate as it will be in 2021. If you could use tax support, let’s chat! We serve individuals, self-employed folks, nonprofit organizations, and small businesses. Here’s Why Cash is King for Your Nonprofit During the 2020/2021 Economic Crisis In our latest blog post, [Chills, Thrills, and Dollar Bill, Part 1] we talked about what a cash flow is, and why it's important for your nonprofit. Now let's dive deeper into 12 ways to steward your organization’s position during tough times.

Revenue Automate earned revenue whenever possible. If you’re collecting fees from individuals for a service, you should be automating that process! Why? It’s key to keeping your cash flow level.

Don’t expect pre-2020 levels of institutional funding to return for a while. Word on the street is not to expect grant funding to return to normal in 2021. Understand that your development team’s attention might be better spent on cultivating other sources of revenue besides grants. Now is the time to try new things. Innovate, test, adapt, test and repeat! Most organizations have some room to deliver an earned revenue model to their constituents. You can no longer afford to wait to diversify your funding streams. Expenses Analyze expenses but don’t analyze to death. What matters is how you deliver on mission. Don’t get analysis paralysis. Know your major buckets of expenses and be prepared to make strategic spending decisions. Know the difference between ROI (return on investment) and ROS (return on scarcity). ROS is a really interesting way to say opportunity cost. Scarcity is a lack of something; nonprofits often suffer from a “scarcity mindset.” So as you look at your spending, consider: if you choose not to fund certain activities due to concerns around scarcity, what opportunities are being lost as a result? Are you eliminating something from your budget that results in a negative impact to your mission? Protect Your Cash on Hand. The following tips might seem a little obvious or like a “Risk Management 101” but they are great reminders. Pay down credit card debt. Organizational credit card debt can really hamstring your ability to save for the future. Wherever possible, if cash allows, pay down your credit cards to avoid paying overly high interest rates. Obtain line of credit. If you already have a line of credit, KUDOS! But use cautiously. Remember it's a loan you have to pay it back. Right now we're seeing some lending happening at the community bank and credit unions level, but the larger banks are not being so generous. If you can obtain a line of credit, even if it’s small, that could help you get by. Determine when to use EIDL funds. If you took an Economic Injury Disaster Loan in 2020, proceed with caution. Think of your EIDL money as an internal line of credit. Sit on the money as long as you can and see if you need it. If you’re going to draw on it, have a plan for how you will repay the funds. EIDL funds are still loans. So you and your board should tap into those funds carefully. Understand FDIC insurance limits on bank accounts. The Federal Government ensures up to $250,000 in bank accounts, so if your organization has more than that in any single bank account, the balance is unprotected. If you want to mitigate that risk, talk to your bank about where you can move your funds to be protected. Manage risk to investments; focus on capital preservation. You might have already done this in 2020 but talk to your investment advisors and find out more about your asset allocation and the risk exposure for your organization’s investments. Pro tip: Keep your board in the loop-they have ultimate fiduciary responsibility for your nonprofit. They are on the hook financially and legally, so make sure your board is on board at all times. To quote Yogi Berra, “if you don’t know where you are going, you might wind up someplace else.” A keen eye on cash will help you manage your organization more effectively and it will also help your board, leadership and constituents know that you are prepared to move your organization forward regardless of the crazy times we’re living in now. If you’re looking to dive deeper into planning your 2021 budget and cash flow, our friendly team at Blue Fox is here to help! Give us a call at (321) 233-3311 or email us at hello@yourbluefox.com. We’ll get you sorted! Then you can focus on what really matters: your mission and serving your community. You can also schedule a free budget consultation: https://calendly.com/chat-with-chantal Here’s Why Cash is King for Your Nonprofit During the 2020/2021 Economic Crisis The Benjamins. That bankroll. Can you tell we’re talking about CASH? Keeping a keen eye on cash flow goes hand-in-hand with creating a meaningful budget for your organization. [Shameless plug, check out our blog post on How to Create a Fairly Meaningful Budget for 2021]

Our CEO, Chantal Sheehan, at Blue Fox recently spoke on the topic of how cash is king at Nonprofit Hub’s Cause Camp conference in October. Her urgent advice to nonprofits is to pay special attention to cash flow specifically during this economic downturn in order to survive. Why? A cash flow forecast is a projection that shows the strength of your cash position over time. Because a projection like this shows you where you’re going to be in 6, 9, 12, or 24 months from a pure cash standpoint, we feel it’s a nonnegotiable tool. So what does a cash flow forecast look like? The good news is that they aren’t that hard to build most of the time! We typically build our forecasts out in a spreadsheet. Rows detail cash inflows and outflows, and columns list out each month in the period you’re forecasting. So imagine: your current cash position (i.e. balances of all your cash/bank accounts) is at the very top. Then cash inflows (revenue, receipts from invoices, investment income, etc) follow. Finally, your outflows (i.e. expenses, debt payments, capital purchases) are listed at the bottom. For example, say you start with $100,000 in the bank, then you make $50,000 in Month 1, while you spend $25,000 in the same t month. Your cash position at the end of Month 1 would = $125,000. ($100,000 + $50,000 - $25,000) So your cash flow forecast shows you where you started, what money you took in and what went out. This type of projection is extremely useful when built out for 12 months or longer. Pro tip: The most financially stable and sustainable organizations pay attention to cash flow because they know it affects everything from their events to payroll.. Now that we’ve covered the importance of cash flow, we're going to dive deeper in our part 2 of this series and cover 12 ways to steward your organization’s position during tough times. In the mean time, if you’re looking to dive deeper into planning your 2021 budget and cash flow, our friendly team at Blue Fox is here to help! Give us a call at (321) 233-3311 or email us at hello@yourbluefox.com. We’ll get you sorted! Then you can focus on what really matters: your mission and serving your community. You can also schedule a free budget consultation: https://calendly.com/chat-with-chantal As you read, remember that our team at Blue Fox is happy to answer questions, provide assistance with PPP applications and forgiveness, and help your organization navigate the pandemic’s financial challenges. On December 21st, the U.S. Senate and House of Representatives passed the $900 billion COVID-19 relief bill: Consolidated Appropriations Act, 2021. [Warning: it’s 5,593 pages… speed readers only!]

So, what does it mean for you? Here is a brief recap of the key takeaways, as summarized by the Journal of Accountancy. (Yes, we summarized a summary, just for you.) Key takeaways for individuals and self-employed: The Bill:

Key takeaways for small business, nonprofits, not-for-profits: The Bill:

Simplified Application The new COVID-19 relief bill also:

For more details read: COVID-19 relief bill addresses key PPP issues by Journal of Accountancy or visit U.S. Small Business Association PPP Resource Page. Or, Just Ask Blue Fox For Help! Our team is happy to answer questions, provide assistance with PPP applications and forgiveness, and help your organization navigate the pandemic’s financial challenges. Give us a call at (321) 233-3311, schedule a phone call, or email hello@yourbluefox.com. Independent Contractors, Self-Employed, Sole Proprietors - That’s You If 2020 has taught us anything, it’s to prepare for the unexpected. How might you do that? Well if you have recently started a side gig to earn extra income, now is the time to compile your financial information to complete the IRS Form 1040, and we can help you do that!

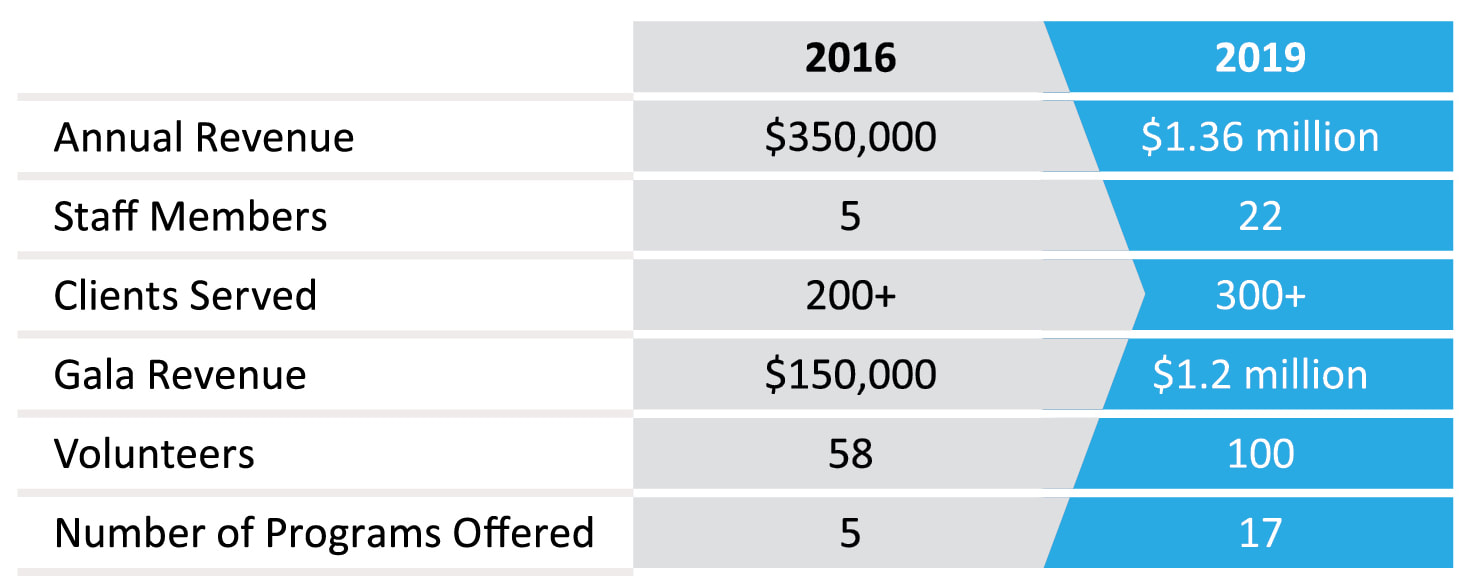

Our foxtastic team at Blue Fox has created multiple resources to help our friends who have a side business [Schedule C Form and Tax Prep video]. We also wanted to share more tips on how to handle taxes for your side hustle. Most people who start a new opportunity invest all their extra time in growing this venture; we’re here to help you with the other fun stuff like taxes. Below are 3 tips on best managing taxes for your side business. 1. Stash cash every payday If you’re used to getting a paycheck from your employer with your taxes withheld, you will have to start taking on that responsibility on your own. Don’t worry, we’ll help you with how much to put aside. In general, put aside 25 to 35 percent of your income. Always make sure to consult with a tax professional [wink wink, us] about how much you’ll need, especially if you are making quarterly payments to the IRS. Small business owners pay quarterly taxes on January 15, April 15, June 15 and September 15. 2. Keep a keen eye on expenses Make sure you are tracking your costs throughout the year. You could do this on your own in a spreadsheet or use something specifically designed for those who are self-employed like QuickBooks Self-Employed to separate business and personal expenses, give you quarterly estimated taxes and automatically track your mileage. Tracking your expenses pays off [literally]. Your professional tax services provider can help show you deductions that you’re eligible for including things like a home-office, mileage, and materials and equipment bought and necessary for your business. 3. Hire a Pro Working with a professional to help you with your tax plan is a great investment in yourself and a new venture. At Blue Fox, we have helped our sole proprietors or single-member LLC clients save thousands of dollars and keep their audit risk low by asking us for help at tax time. Another group of our clients have taken their side hustle to a whole new tax advantaged level by becoming S-corporations. We love using legal strategery (yes, we know that’s not a word) to proactively help people maximize their tax refunds. [Read more about that here.] It wouldn’t be 2020 if there wasn’t complication so we think it’s best to reach out to a tax expert [hey, we would love to help] to ensure you are on the right track with the behind-the-scenes side of your business. If you’re looking for a human person to talk to about tax planning, that’s us. Let’s connect at (321) 233-3311 and hello@yourbluefox.com. Meet One of The Most High-Functioning, Financially Sustainable Nonprofit Organizations We Know: STARability FoundationPage 5 is a must read! A step-by-step financial transformation timeline (blueprint) of how STARability grew their organization and achieved true sustainability.  As most of you know, I like to joke that I'm a recovering nonprofit executive director. I was an ED at the tail end of the Great Recession, and fundraising was still one of the toughest jobs out there. Funders everywhere were talking about nonprofit sustainability, earned revenue models, and diversified revenue streams. I became fascinated with the concept personally and professionally. Is it possible? Or is it just a pipe dream? Fast forward 10 years and I can tell you with certainty: nonprofit sustainability is not a unicorn. There's a process, cycle, and science to it, and we help our clients move in that direction every day. Take a few minutes to read our first ever case study about our amazing client the STARability Foundation and see how their sustainability story unfolded over the last 5 years. And discover the steps that you can take to move your organization toward a more secure future, even in uncertain times. With you, Chantal Sheehan A Note From our Founder & CEO: Sometimes budgets can feel like necessary evils instead of tools (how we think of them). Even scarier is creating a budget for 2021 after 2020’s dumpster fire of a year. Everything is uncertain. So, how can you plan for the future? Our CEO at Blue Fox recently spoke on this topic at Nonprofit Hub’s Cause Camp conference in October. [Video clip below] Here are some small steps to take to create a meaningful budget. 1. Get 2020 financials up-to-date Scrub your data in Quickbooks or in your accounting files and make sure you have accurate data on the books. Having accurate reports is the foundation for good budget planning, which leads us into step #2. 2. Do some math Use our Magical Nonprofit Financial Ratio Matrix to assess your organization’s financial health. This tool will provide you vital information to assist in your budgeting process. Remember: information is NOT insight. Information is data that requires analysis. And, through analysis, your organization can generate insight and inform strategic budget decisions. 3. Review your budget v. actual for 2020 carefully WITH your team Bringing your team into this step of the process is extremely valuable. A lot of times small organizations develop their budget in a vacuum. That makes no sense because your team is your single greatest asset. Your team is your mission. They have their ear to the ground and know exactly what’s happening in their respective department.  4. Determine reasonable assumptions for 2021 You have more information and insight than you probably think! Take the data that you have then make your assumptions as broad as you can. 5. Evaluate the key drives/levers of revenue and expenses What factors ramp up or ramp down revenue? What are the expenses that are key to keeping your organization afloat or on target? 6. Think about long-term vs. short-term needs; the short-term focus is OK right now Right now a short-term focus is OK. When you look at your budget, 12 months is plenty. you don’t have to forecast beyond that right now. For a lot of our clients this year, things have changed month-to-month, even day-to-day. Don’t worry so much to project your long-term budget just focus on the next 12 months. Some of our clients are currently reviewing their budget every month. They are not formally changing it but having conversations with their finance committee about what’s happening day-to-day and month-to-month. That way they have a really keen understanding of levers and drivers of their financial sustainability. And, they can proactively find solutions to challenges that pop up. 7. Determine decision-making budget moments in 2021 Scenario planning is key! Decision-making moments are preset moments in times, activities, in regard to revenue or expense metrics at which you will make a certain decision. Say you have an annual signature event but because of COVID, this annual event is now held virtually. How are you supposed to know how much money the event will raise now that it’s not in-person? You don’t! You can just hope and guess. What will you do if revenue is significantly lower? What if your expenses change? It’s impossible to predict what’s going to happen in 2021. That’s why having preset triggers set in your budget will help your leadership team make decisions as the year unfolds. More Budget Pro Tips:

Budgeting for a shortfall This might sound like a radical and crazy idea coming from an accounting firm but consider budgeting for 2021 to be in the red. Say whaaaaat? Think about it: Everything is unknowable. Revenue targets are going to shift. Expenses could go up or way down. You’re going to build a budget that’s the best idea from the information you have right now. But why build a budget that has overly rosey revenue predictions just so you can say it’s balanced? Don’t do that to your organization. Plan with the caveat that if you have cash and the financial runway to do so go ahead and plan for some shortfall. We are currently advising clients right now that no more than 15% of your budget should be in the red. Nonprofits do not need to have a balanced budget under these circumstances, assuming you have the cash to sustain your position through that shortfall for the next year. Looking to dive deeper into planning your 2021 budget? Our friendly team at Blue Fox is here to help! Give us a call at (321) 233-3311 or email. We’ll get you sorted! Then you can focus on what really matters: your mission and serving your community. You can also schedule a free budget consultation: https://calendly.com/chat-with-chantal  As if this year hasn’t been crazy enough, navigating through the Paycheck Protection Program (PPP) is also an eyebrow raiser. The big question lately is when to submit the loan forgiveness forms (3508, 3508EZ, and 3508S)? If you’re fearful that you might miss the 11/30/2020 deadline–which is displayed in the upper-right corner of the forms–don’t worry, we have good news for you!

The U.S. Small Business Administration (SBA) recently released a new entry in the loan forgiveness FAQs document addressing, “Is November 30, 2020 the deadline for borrowers to apply for forgiveness?” The answer is no. Borrowers can submit a loan forgiveness application any time before the maturity date of the loan, which is either two or five years from the loan origination. If you’re like me and wondering, “Well then why the heck is that date printed on the loan?” The reason for the expiration date in the upper-right corner is for the SBA’s compliance with the Paperwork Reduction Act and it reflects the temporary expiration date for approved use of the forms. Here’s another insider tip: the accounting lobby is currently advising businesses and nonprofits to WAIT to submit their loan forgiveness applications until Congress takes up a bill called the Paycheck Protection Small Business Forgiveness Act. This bill would create an easy, almost ‘automatic’ form for loan forgiveness for loans under $150,000. Now wouldn’t that be nice?! So if your PPP loan was less than $150,000, we recommend you sit tight until this bill is addressed by Congress. To read more helpful FAQ on PPP from the SBA, check it out here. As always, our team is happy to answer questions and help your organization navigate current financial challenges. Give us a call at (321) 233-3311 or email hello@yourbluefox.com. |

Our BlogWelcome to the Blue Fox Blog! A fairly entertaining source of info and news related to our company, nonprofits, social sector trends, and, of course, accounting. Enjoy! Top ArticlesBack to Basics: How to Set Up Your Nonprofit Chart of Accounts

How "Small" Payroll Mistakes Cause Multi-Year S#!t Storms for Nonprofits Behind the Scenes, New Client Onboarding Call When to Hire a Tax Professional - 10 Factors to Consider 40+ Ideas to Light a Fundraising Fire Under Your Nonprofit Board Members Why Outsource Your Nonprofit Accounting to Blue Fox? Ask One of Our Newest Clients Client CASE STUDY: One of The Most Financially Sustainable Nonprofit Orgs We Know The Magical Nonprofit Financial Ratio Matrix 10 Reasons to Outsource Your Nonprofit Accounting How to Make Your Nonprofit Recession-Proof How to Engage Your Board of Directors in Financial Conversations QB Tip of the Month: How to Use Classes for Painless Grant Writing When to Hire an Accountant for Your Social Impact Org Are You Paying Too Much for Payroll? Company NewsBlue Fox Teams Up With Bloomerang to Develop Nonprofit Resources

Blue Fox Earns Better Business Bureau Accreditation Blue Fox Launches Protected By Logo Blue Fox - The Origin Story Categories

All

Archives

June 2023

|

RSS Feed

RSS Feed

|

|

BLUE FOX

Phone: (321) 233-3311, Email: hello@yourbluefox.com

Mailing Address: 2542 Woodfield Circle, Melbourne, FL 32904

Copyright © 2024 - All Rights Reserved

Holiday office closures: To give our employees time to unplug and refresh with their family and friends, the Blue Fox virtual office closes

for all federal holidays, the week of Thanksgiving, and the week between Christmas and New Year's Day.

Phone: (321) 233-3311, Email: hello@yourbluefox.com

Mailing Address: 2542 Woodfield Circle, Melbourne, FL 32904

Copyright © 2024 - All Rights Reserved

Holiday office closures: To give our employees time to unplug and refresh with their family and friends, the Blue Fox virtual office closes

for all federal holidays, the week of Thanksgiving, and the week between Christmas and New Year's Day.